Cross-Selling & Up-Selling in Motor Insurance

Motor insurance is a mandatory product—but selling only the basic policy means missing opportunities to add value for customers and grow business. That’s where cross-selling and up-selling come in. The IC-72 text emphasizes their importance in helping insurers increase revenue while giving customers better protection.

🔎 What is Cross-Selling?

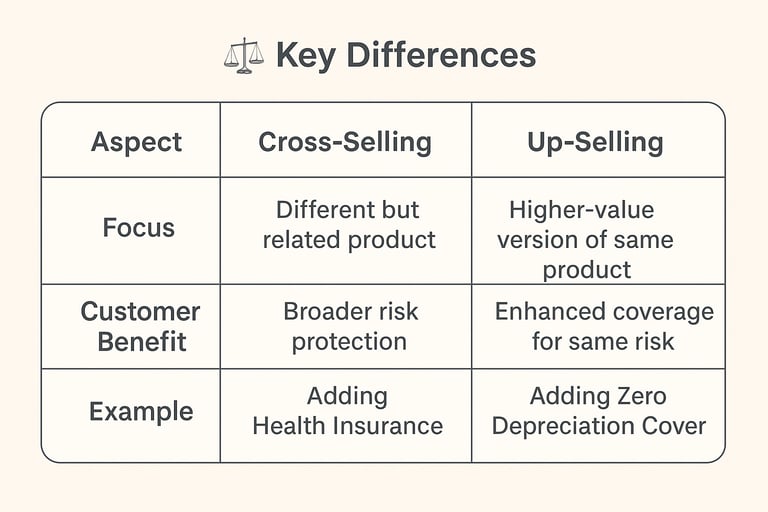

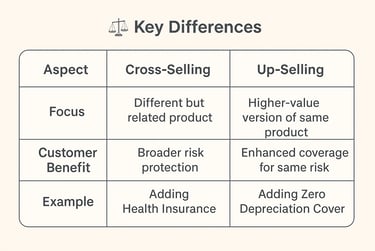

Cross-selling means offering related insurance products that complement the motor policy.

Examples of Cross-Selling in Motor Insurance

Selling Personal Accident Insurance to car/bike owners.

Offering Health or Travel Insurance at the time of motor policy renewal.

Recommending Household or Fire Insurance for customers buying a motor policy.

👉 Scenario: A customer insures his car. The agent cross-sells a personal accident policy, covering medical expenses in case of a road accident.

🔎 What is Up-Selling?

Up-selling means persuading the customer to buy a better or higher-value version of the same product.

Examples of Up-Selling in Motor Insurance

Suggesting a Comprehensive Policy instead of just Third-Party Liability.

Adding Zero Depreciation, Engine Protection, and Roadside Assistance add-ons.

Advising Return to Invoice Cover for new cars.

👉 Scenario: A customer asks for a third-party only policy (cheaper). The agent explains benefits of a Comprehensive + Zero Dep policy, leading to higher coverage and premium.

⚖️ Key Differences

✅ Why Cross-Sell & Up-Sell?

For Customers:

Comprehensive protection.

Peace of mind in multiple risk areas.

For Agents/Insurers:

Higher premium income.

Better customer retention.

Increased trust as a one-stop risk advisor.

💡 Sales Tips for Agents

Educate, Don’t Push – Customers buy when they understand the value.

Use Real-Life Examples – “Imagine your new car gets stolen. Return-to-Invoice Cover ensures you get full invoice value—not depreciated IDV.”

Bundle Smartly – Offer packages (Car Insurance + PA Cover + Roadside Assistance).

Timing Matters – Best opportunities: new purchase & renewal time.

Digital Tools – Use premium calculators to show difference in protection vs. premium.

🎯 Conclusion

Cross-selling and up-selling are not about forcing extra products—they are about being a true advisor. By recommending the right covers and related products, agents help customers stay secure while strengthening their own business.

👉 Pitch Line for Agents:

“Don’t just sell insurance. Sell peace of mind. Cross-sell to broaden protection, up-sell to enhance coverage.”