How IDV (Insured Declared Value) is Calculated in Motor Insurance

When customers buy or renew motor insurance, one of the most important terms they hear is IDV – Insured Declared Value. For many, it sounds confusing. But as an agent, if you can explain IDV clearly, you’ll build credibility and trust.

🔎 What is IDV?

IDV = Current Market Value of the Vehicle.

It represents the maximum amount the insurer will pay in case of total loss or theft.

IDV also forms the basis for calculating the Own Damage (OD) premium.

👉 Think of it as the sum assured of the vehicle policy.

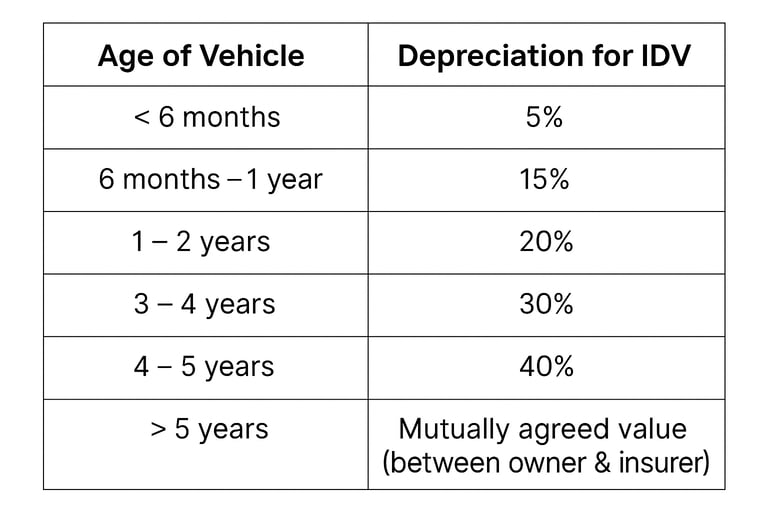

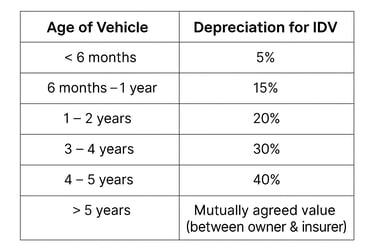

📉 How is IDV Calculated?

Start with Manufacturer’s Ex-Showroom Price (listed selling price of the same model and variant).

Registration cost and road tax are not included.

Apply Standard Depreciation as per Vehicle Age:

Add Cost of Accessories (not part of manufacturer’s price).

Example: music system, alloy wheels, CNG kit.

📊 Example: IDV Calculation

Car: Hyundai Creta Petrol (Ex-Showroom Price ₹10,00,000)

Age: 2 years

Accessories added: Alloy wheels worth ₹50,000

Step 1: Apply Depreciation

Depreciation rate for 2 years = 20%

Depreciation = 20% of ₹10,00,000 = ₹2,00,000

Value after depreciation = ₹8,00,000

Step 2: Add Accessories Value

₹8,00,000 + ₹50,000 = ₹8,50,000

✅ Final IDV = ₹8,50,000

This becomes the maximum claim amount if the car is stolen or declared a total loss after an accident.

❌ Common Misconceptions

IDV is not resale value – It is the insurer’s liability limit, not the car dealer’s buyback price.

Lower IDV doesn’t mean savings – A lower IDV reduces premium but also reduces claim payout.

Higher IDV doesn’t always help – Inflating IDV means higher premium; claims are still settled at actual market value.

💡 Sales Tips for Agents

Explain Trade-Off Clearly – Higher IDV = Higher premium but better protection.

Use Real-Life Scenarios – “If your car worth ₹8 lakh is stolen, do you want to get only ₹6 lakh or the correct IDV of ₹8.5 lakh?”

Advise Fair IDV – Guide customers to choose a realistic IDV, not too low or too high.

Cross-Sell Add-Ons – Add-ons like Return to Invoice Cover enhance claim payout beyond IDV for new cars.

✅ Conclusion

The IDV is the backbone of motor insurance—it directly impacts both premium and claim settlement. For agents, explaining IDV with simple examples builds trust and helps customers make informed choices.

👉 Pitch line for customers:

“Your IDV is the true value of your car today. It decides both what you pay as premium and what you’ll get in case of total loss. Let’s set it right for your peace of mind.”