🚗 Purpose & Benefits of Motor Insurance for Customers

Motor insurance is more than just a legal formality — it’s a shield that protects both the vehicle owner and others on the road. For customers, it offers financial security, legal compliance, and peace of mind. Let’s understand the why and how behind it.

1️⃣ Purpose of Motor Insurance

1. Legal Requirement

In India, Third-Party (TP) Insurance is compulsory under the Motor Vehicles Act, 1988. Without it, driving on public roads is illegal.

Note: Third-Party Insurance – Covers injury, death, or property damage caused to someone else by your vehicle.

2. Financial Protection for the Vehicle Owner

An Own Damage (OD) Cover safeguards the insured’s own vehicle against losses from accidents, theft, fire, or natural calamities.

Note: Own Damage Cover – Policy section that pays for repairing or replacing your own vehicle.

3. Compliance with Permit & Registration Rules

Motor insurance is linked to the registration of vehicles and the permits for transport vehicles, ensuring lawful use.

4. Protection Against Liabilities

Covers legal liabilities arising from injury or death of third parties or damage to their property.

Note: Legal Liability – A responsibility imposed by law to compensate another person for harm or loss caused.

2️⃣ Types of Motor Insurance Policies

1. Own Damage (OD) Cover – Protects the insured’s own vehicle against loss/damage.

2. Third-Party (TP) Liability Cover – Covers injury, death, or property damage to others.

3. Comprehensive/Package Policy – Combines OD + TP.

Exam Note: “Act Policy” usually means only TP cover as per Motor Vehicles Act.

3️⃣ Key Principles in Motor Insurance

Motor insurance is governed by general insurance principles plus legal requirements:

Utmost Good Faith – Full disclosure of facts by the proposer.

Insurable Interest – The insured must stand to lose financially if the vehicle is damaged or lost.

Indemnity – Compensation to restore the insured’s financial position without profit.

Subrogation – Insurer’s right to recover loss amount from third parties after claim payment.

Contribution – Loss shared proportionately between insurers if double insurance exists.

Proximate Cause – Loss must be directly caused by an insured peril.

4️⃣ Legal Requirements Under MV Act, 1988

Compulsory TP cover before using a vehicle in public.

Certificate of Insurance (Form 51) must be issued.

Transfer of policy on sale of vehicle → TP section automatically transfers; OD section needs insurer consent within 14 days.

Permits & Fitness Certificates are essential for transport vehicles.

Exam Tip: Remember Section 146 (Compulsory Insurance) & Section 157 (Transfer of Insurance)

5️⃣ Industry Snapshot

Loss ratio for motor insurance in 2021–22: 81.3% (IRDAI data).

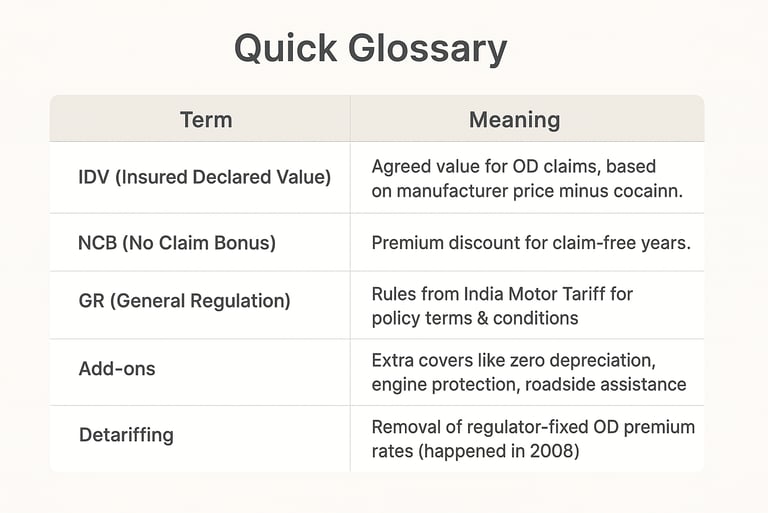

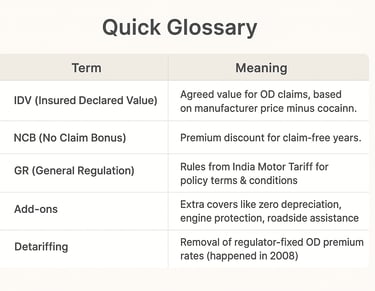

TP premium rates fixed by IRDAI; OD rates are market-driven (since 2008 detariffing).

Growth drivers: electric vehicles, online distribution, vehicle scrappage policy.

🎯 Memory Hooks for Exam

“TP is Law, OD is Choice” – Remember which is compulsory.

“IDV is Agreed, not Market Price” – IDV is fixed at policy start.

“14 Days for OD Transfer” – After vehicle sale.

“MV Act 146 & 157” – Compulsory insurance & transfer rules.