📊 The Law of Large Numbers – The Backbone of Insurance

🌟 Why This Concept Matters

Have you ever wondered how insurance companies manage to pay huge claims — sometimes in crores — even when the premiums they collect from individuals are small?

How can they afford to do that and still remain profitable?

The answer lies in one powerful mathematical truth — The Law of Large Numbers.

It’s the invisible engine that keeps the entire insurance system running smoothly.

🔍 What Is the Law of Large Numbers?

Let’s start simple.

The Law of Large Numbers (LLN) says:

“When the number of similar events or trials increases, the actual results get closer to the expected results.”

In plain English, the bigger the group you study, the more accurate your predictions become.

🪙 A Simple Example

Let’s say you toss a coin.

The chance of getting heads is 50%.

Now toss it 10 times — you might get 7 heads.

Toss it 100 times — you might get 48 or 52 heads.

Toss it 10,000 times — you’ll get very close to 5,000 heads.

The more times you toss the coin, the more predictable the result becomes.

That’s the Law of Large Numbers in action.

🏦 How It Applies to Insurance

In insurance, every policyholder represents a “trial.”

No one can predict who will have an accident, fall ill, or lose property — but insurers can estimate how many people (out of a large group) are likely to experience these events.

Example 👇

If 10,000 people buy motor insurance:

Not everyone will have an accident.

But based on past data, the insurer might estimate that around 3% (i.e., 300 people) will file claims.

Because they know roughly how many claims to expect, insurers can calculate premiums that are:

Fair for customers

Sufficient to cover future claims

Profitable for the company

So, by observing a large number of similar risks, insurers can predict losses more accurately.

That’s why it’s called the backbone of insurance.

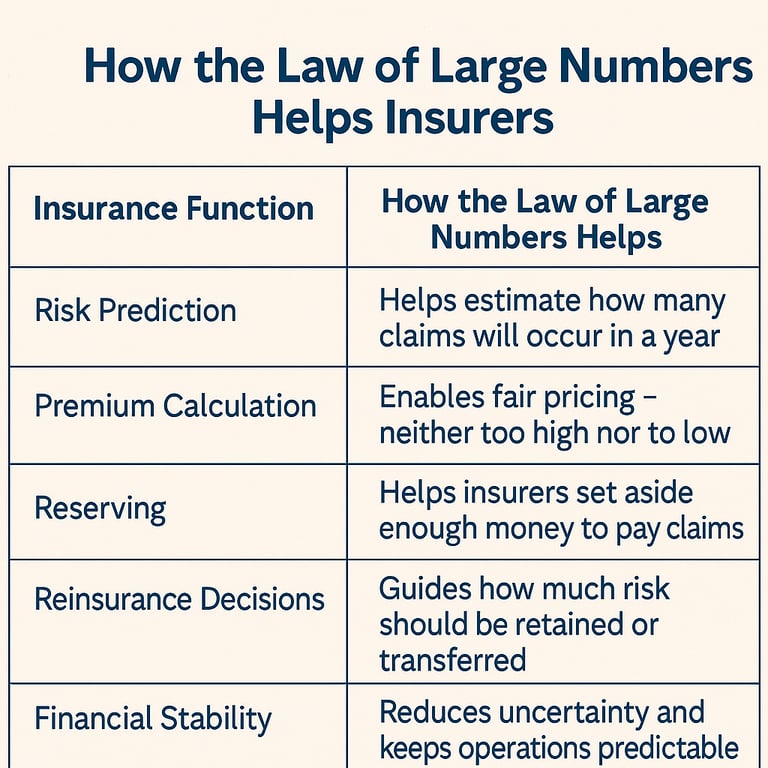

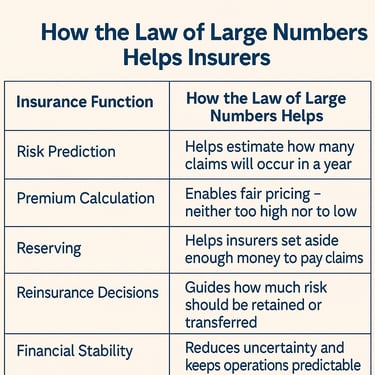

⚙️ How the Law Helps Insurers

Here’s how the Law of Large Numbers supports every step of the insurance business:

🧮 The Math Behind the Magic (Simplified)

Let’s use a basic illustration:

Suppose each of 1,000 similar houses has a 1% chance of catching fire in a year, with an average loss of ₹5 lakh per house.

That means, statistically, 10 houses (1% of 1,000) will suffer fire loss:

👉 Total expected loss = 10 × ₹5,00,000 = ₹50,00,000

If the insurer collects ₹6,000 as premium per house:

👉 Total premium = 1,000 × ₹6,000 = ₹60,00,000

Even after paying ₹50,00,000 in claims, the insurer still has enough to cover expenses and profit.

However, this calculation works accurately only when the group is large.

If only 10 houses were insured, and 2 caught fire, the results would be disastrous.

That’s exactly why insurance companies always seek to spread risk across a large number of similar exposures.

⚠️ What Could Go Wrong

The Law of Large Numbers works beautifully — but only under certain conditions:

1️⃣ The group must be large enough.

Small numbers give unstable, unpredictable results.

2️⃣ The risks must be similar.

Pooling dissimilar risks (like mixing homes and factories) leads to wrong estimates.

3️⃣ Past must resemble the future.

Sudden changes — like a pandemic, war, or new technology — can make past data unreliable.

4️⃣ Randomness is key.

Losses must occur by chance, not by intention or pattern.

🔐 How Insurers Manage Uncertainty Despite It

Even with this law, insurers know predictions are not perfect. So, they:

Use actuarial models to refine estimates.

Purchase reinsurance for catastrophic losses.

Build reserves for emergencies.

Analyze data regularly to update pricing.

Use technology and AI to track trends faster than ever before.

This ensures that even if some years bring more losses, the company remains stable over time.

💬 Real-Life Example

Think of a health insurance company.

It doesn’t know who will fall ill next year — but with data from millions of people, it can predict how many will need hospitalization, what the average cost might be, and how much premium to collect.

Without such predictions, insurance would be nothing more than a gamble.

🧠 Quick Recap

The Law of Large Numbers means: The larger the group, the more predictable the outcome.

It allows insurers to estimate future losses, set fair premiums, and stay financially sound.

The law only works when risks are similar, independent, and numerous.

It turns uncertainty into measurable, manageable risk — and that’s the magic of insurance.

🧾 Key Takeaways for Agents & Students

✅ Insurance survives on collective sharing — made possible by LLN.

✅ LLN helps insurers predict “how many,” not “who.”

✅ Larger and more homogeneous the pool, better the prediction.

✅ For exams — remember:

“The Law of Large Numbers reduces uncertainty by converting random individual risks into predictable group outcomes.”

✅ For clients — you can explain it simply as:

“Insurance works because many people contribute, but only a few actually claim.”