💡 Understanding Insurable Interest and Why It Matters

🌟 Introduction

Imagine you buy a life insurance policy for a stranger you’ve never met.

If that person dies, you get the money.

Sounds wrong, doesn’t it?

That’s exactly why Insurable Interest exists — it ensures insurance remains a tool of protection, not speculation.

This principle keeps insurance ethical, legal, and fair. Without it, insurance could easily turn into gambling.

🔍 What is Insurable Interest?

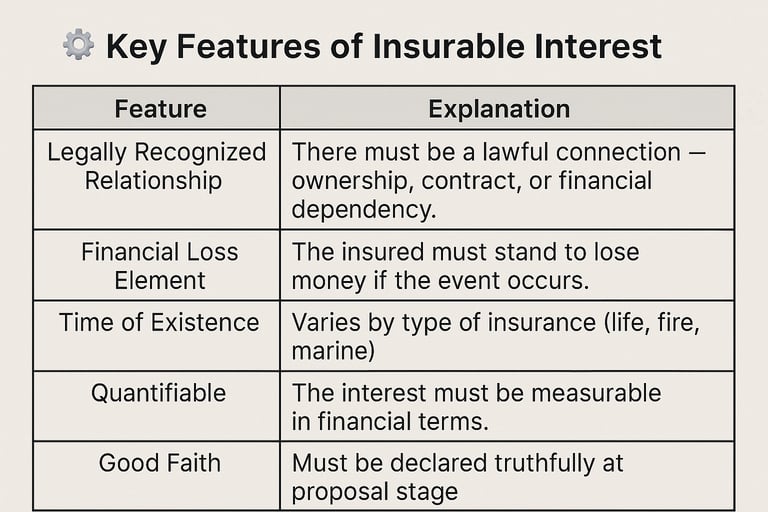

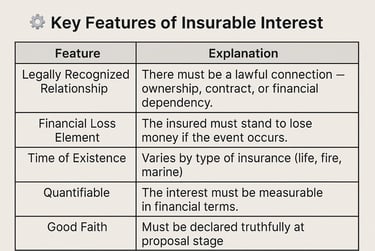

Insurable Interest means that the person buying insurance must have a financial relationship with the subject of insurance — a relationship such that they will suffer a financial loss or emotional hardship if the insured event happens.

In simple words:

“You can insure only what you stand to lose.”

If there’s no potential for loss, there’s no reason for insurance.

🏦 Definition (Simplified)

Insurable Interest is the legal right to insure arising from a financial relationship recognized by law between the insured and the subject matter of insurance.

This principle ensures that the insured person has a genuine stake in the preservation of the insured life, property, or event.

🧩 Why It Matters

Without insurable interest, anyone could take out insurance on another person’s life or property, hoping something bad happens so they can profit.

That’s not insurance — that’s betting on loss.

Insurable interest keeps insurance honest, moral, and lawful by making sure:

1️⃣ The policyholder actually faces a loss.

2️⃣ The insurance company compensates genuine damage, not speculative bets.

3️⃣ The insurance contract stays legally valid.

⚖️ Legal Importance

Under Section 30 of the Indian Contract Act, 1872, wagering (betting) contracts are void.

Insurance contracts are not wagers because they are based on insurable interest.

This means that the insured must have something to lose if the insured event occurs.

If no insurable interest exists — the policy becomes void and unenforceable in court.

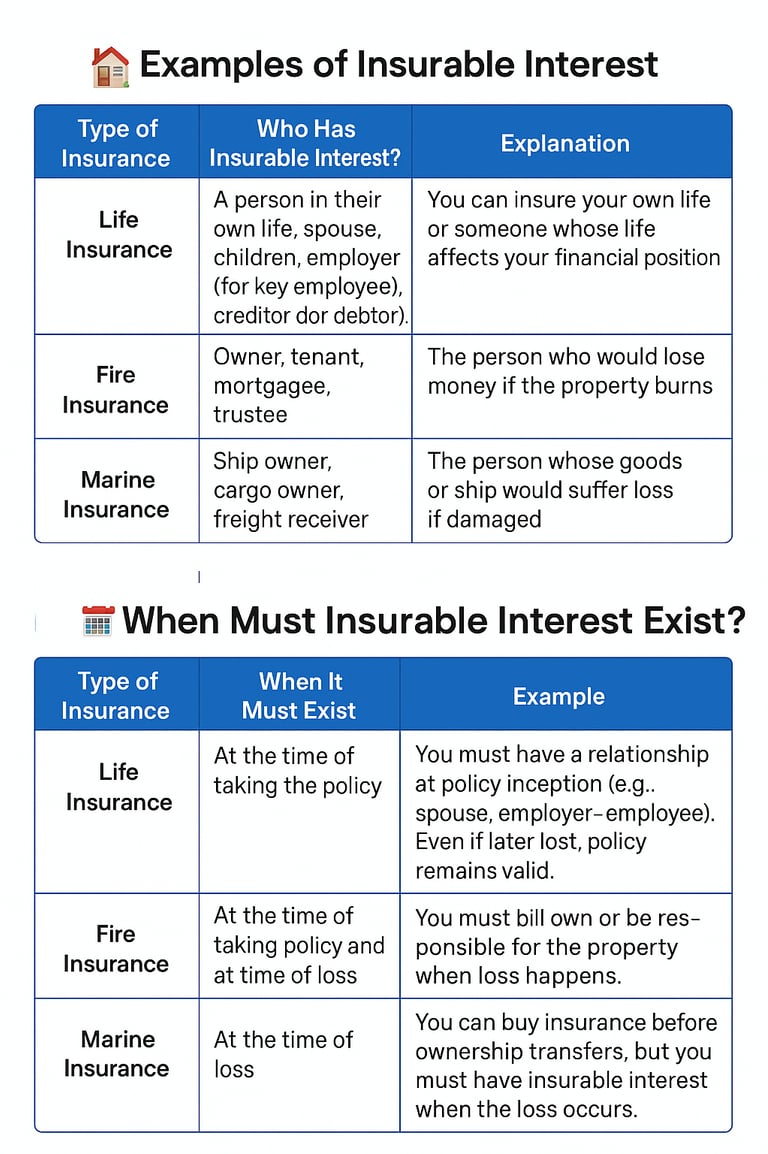

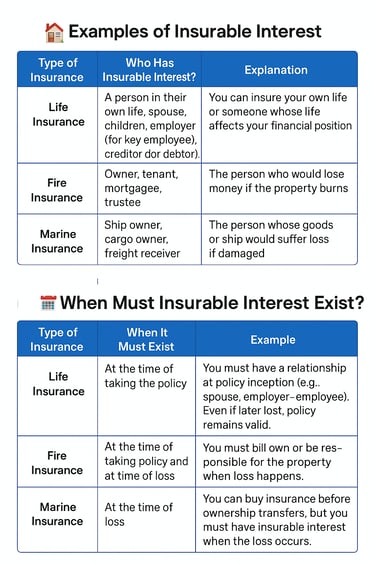

💬 Real-Life Examples

1️⃣ Life Insurance

A husband buys life insurance on his wife’s life. He has an insurable interest because her death would cause both emotional and financial loss.

But if he tries to insure a stranger’s life — no insurable interest exists, and the contract is void.

2️⃣ Fire Insurance

A shop owner insures his store. Later, he sells it but forgets to cancel the policy.

If a fire occurs after the sale — he no longer has ownership, so no insurable interest, hence no claim.

🚫 When Insurable Interest Is Missing

Without insurable interest:

The contract becomes void.

The insurer can refuse the claim.

The insured could be seen as betting on loss.

For example, if someone insures a celebrity’s life without connection or consent — that’s not insurance, it’s gambling.

🧠 Quick Recap

Insurable Interest = Legal & Financial Connection to the Subject of Insurance.

Ensures only genuine losses are compensated.

Prevents insurance from becoming gambling.

Must exist at specific times depending on the type of insurance.

Without it, the policy is void and unenforceable.

💡 Key Takeaways for Agents

✅ Always verify whether the proposer has a genuine financial relationship with the subject matter.

✅ Remember for exams:

“Insurance is not valid without Insurable Interest.”

✅ Educate clients — insurance protects what you own or depend on, not something random.

✅ In fire and marine insurance, double-check ownership and responsibility before issuing cover.